The amount of time to obtain your bond depends on several different variables. The most important being how long it takes you to respond to what is needed. The faster you get your agent the information they need to write the bond, the faster they can send it up to the bonding company for approval. Of course there are other variables, such as how busy the bonding company’s underwriters are at any given time. At Bernard Fleischer & Sons, Inc. we make sure to process your bond as fast as possible.

All posts by BFBOND

How much do surety bonds cost?

Surety bond premiums vary from one surety to another, but can range from one-half of one percent to two percent of the contract amount, depending on the size, type, and duration of the project and the contractor. In many cases, performance bonds incorporate payment bonds and maintenance bonds. When bonds are specified in the contract documents, it is the contractor’s responsibility to obtain the bonds. The contractor generally includes the bond premium amount in the bid and the premium generally is payable upon execution of the bond. If the contract amount changes, the premium will be adjusted for the change in contract price. Payment and performance bonds typically are priced based on the value of the contract being bonded, not necessarily on the size of the bond. Commercial bonding has a greater range of pricing; high risk programs have a high premium and 10% collateral.

How does a bonding agency underwrite?

A surety company must determine the probability of a loss should the principal be unable to complete their obligations under the bond. Since a bond is an extension of credit, the surety company must analyze the principal’s financial standing and business aptitude to determine if the principal has the financial strength and business knowledge to support the bonded obligation. This is called the underwriting process. Surety company underwriters evaluate risks in ways similar to banks evaluating loan applications. Underwriters consider business and personal financial statements, credit reports, credit references and other factors.

What is a surety bond, anyway?

A Surety Bond guarantees the fulfillment of a legal obligation. It’s a three-party agreement where the third party (surety company) guarantees to a second party (obligee or owner) the successful performance of the first party (principal). One of the primary uses of bonds today is to protect public and private funds from financial loss.

A surety bond is not an insurance policy. An insurance policy assumes that there will be a loss, so the premium for an insurance policy is calculated to cover losses that will occur. A bond, on the other hand, is an extension of credit with the assumption that the legal obligation will be fulfilled, and consequently, there will be no loss. The bond premium paid to the surety covers only the underwriting expenses of the surety company. When losses occur, they have a significant impact on the surety company’s financial results.

Why would an administration bond have a fixed amount?

One reason, an adminsistrator Bond is required, is the estate might appreciate in value, additional assets may be discovered but not reported to the court. This is not at all uncommon, it may be inconvenient to report. The fiduciary may deliberately fail to report in order to avoid having the bond increased and to avoid additional premium and cost. Whether the additional bond is furnished or not, the surety is liable up to the amount of the loss, but not in excess of its bond penalty. Therefore, the proper basis of premium computation is the amount of the bonds, not the amount of the personal property.

How does one become a bonded administrator?

The administrator is generally the choice of the family of the deceased, and is chosen because they believe he or she is the most able among them. Since they know him or her better than anyone else, it usually works out that a person appointed to handle an estate is a good sort of risk.

Before he commences his task of collecting all of the moneys due the estate, he must furnish a bond, which guarantees that he will faithfully perform his duties as administrator, that he will file inventory within a short period, pay claims, distribute the residue in accordence with the law and last but not least make proper return to the court by a final accounting, covering everything that has been done. When the court has approved what has been done, then his bond to the surety can be released.

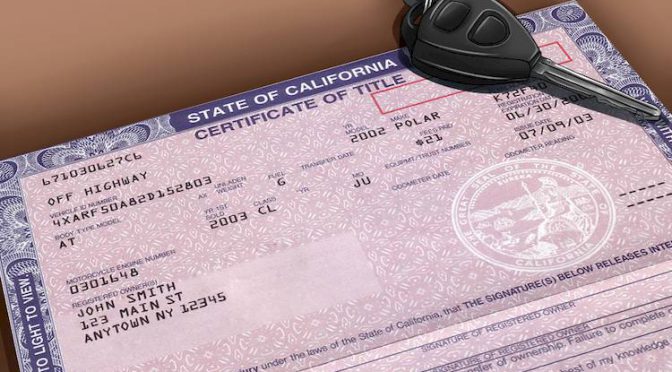

What are title bonds?

While reading quick summaries of different kinds of bonds, I paused on the description of title bonds. I think they illustrate well the basic idea behind bonds, and how they act as a mechanism of trust between two parties.

Title bonds are required usually by state governments before they will reissue titles for larger items like cars. They bond you to your claim that you have legitimate ownership of the item in question, so that people can’t just go around stealing things and filling out some paperwork to have it legally defined as theirs.

For instance, let’s say you lost your copy of the title to your truck that you bought from that shady little used car lot way out of town. Maybe you never got a proper title from the dealership; they didn’t have one at the time, they said, and a bill of sale would be just as good. After a few years, you decide to sell it, but the buyer says that a bill of sale is not enough, that you will need to get a title to transfer to him. You try to find the dealership to get a copy, but find out that they went out of business, got shut down for “correcting” their lot’s odometers, and that no trace of them remains.

Now, in order to get a title reissued by the state, you will need to buy a title bond from a bonding agency like Bernard Fleischer & Sons. The state will generally decide how much we will have to write the bond for. That bond will guarantee any damage done to the car while it is in your possession, in the event that a more legitimate title-holder materialized later on. Perhaps you discover that your dealership was “correcting” ownership on their cars as well as mileage. Now you just have to hope that the shady dealership way out of town had posted a Motor Vehicle Dealer Bond.

What is a Fiduciary?

A Fiduciary is a person appointed to handle the affairs of another who, for one reason or another is unable to handle their own affairs. If the reason is the person is a minor, the fiduciary is called a guardian. When the reason is death, the court appoints an administrator. If the deceased has left a will, naming some person to be the administrator, the court usually permits that person to qualify as an executor.

If the reason is mental incompetence, physical disability, inability to conserve his own assets, the fiduciary is called a committee, a conservator or a guardian.

When a businessman’s financial affairs become involved, an assignee for the benefit of the creditors is named. If placed in a receivership a fiduciary is known as a receiver.

Please note: Fiduciaries are usually required by statute to furnish bonds, conditioned on faithfully performing their duties in the appointed capacities.

What are Court Bonds?

Court Bonds can be the most confusing kinds of bonds. Here’s what I’ve made out of the confusion:

Court Bonds relate to court proceedings, all of which involve two parties: the plaintiff and the defendant. So it makes sense that court bonds are divided into two categories: Plaintiff’s Bonds and Defendant’s Bonds. Both of these bonds are required as protection for the other party. Plaintiff’s bonds protect the defendant–bond the plaintiff to the defendant’s protection, if you will–and defendant’s bonds protect the plaintiff.

An example of a Plaintiff’s Bond–one specifically called an attachment bond–would be if the plaintiff was claiming that the defendant owed him, say, several thousand dollars. The plaintiff could “attach” something like the defendant’s car so that, if the court ruled in the plaintiff’s favor, the defendant’s car could be sold to pay the plaintiff his money. The problem with this is that the court may not rule with the plaintiff, which would be depriving the defendant of his car for no good reason. The plaintiff’s bond assures that the defendant will be compensated for his loss, perhaps at the plaintiff’s expense.

An example of a Defendant’s Bond–one specifically called a garnishment bond–would be if the plaintiff, let’s say a car dealership, sold the defendant a car, to be paid for in monthly installments. If the defendant then didn’t pay his bills from the dealership, they could ask the courts for the power to “garnish” the money straight out of the defendant’s salary. However, it’s possible that the court might not allow the dealership to garnish the defendant’s salary, and maybe instead would tell them to just take back the car. The the dealership therefore has to buy a garnishment bond promising that they will cover whatever losses the defendant sustained from his salary being garnished, if it turns out that they’re just going to repossess the car.

When you’re buying a home, consider the cost of homeowners insurance.

You may pay less for insurance if you buy a house close to a fire hydrant or in a community that has a professional rather than a volunteer fire department. It may also be cheaper if your home’s electrical, heating and plumbing systems are less than 10 years old. If you live in the East, consider a brick home because it’s more wind resistant. If you live in an earthquake-prone area, look for a wooden frame house because it is more likely to withstand this type of disaster. Choosing wisely could cut your premiums by 5 to 15 percent.

Check the CLUE (Comprehensive Loss Underwriting Exchange) report of the home you are thinking of buying. These reports contain the insurance claim history of the property and can help you judge some of the problems the house may have.

Remember that flood insurance and earthquake damage are not covered by a standard homeowners policy. If you buy a house in a flood-prone area, you’ll have to pay for a flood insurance policy that costs an average of $400 a year. The Federal Emergency Management Agency provides useful information on flood insurance on its Web site at www.fema.gov/nfip. A separate earthquake policy is available from most insurance companies. The cost of the coverage will depend on the likelihood of earthquakes in your area.

In California the California Earthquake Authority (www.earthquakeauthority.com) provides this coverage.

If you have questions about insurance for any of your possessions, be sure to ask your agent or company representative when you’re shopping around for a policy. For example, if you run a business out of your home, be sure to discuss coverage for that business. Most homeowners policies cover business equipment in the home, but only up to $2,500 and they offer no business liability insurance. Although you want to lower your homeowners insurance cost, you also want to make certain you have all the coverage you need.>